Fall In Love with the Perfect House For You

Good Monday Morning! The Real Estate market in the Eugene and Springfield area remains extremely favorable for home buyers. With low mortgage interest rates hanging around and great home values, the climate is perfect for a home purchase. The following is an article from Realty Times that gives some good advice to home buyers.

Finding a home is a lot like finding your true love. Love makes your heart skip a beat. Your feet immediately start to spin around the empty living room and imagine yourself entertaining grandly as you waltz through the dining room. And by the time you get to the master bedroom, well….it's love.

But if you've ever been in a bad relationship, you know it can start with that head over heels feeling. You remember that feeling. It's the one that makes you do stupid things that you regret later, like blithely overlooking flaws you wouldn't have put up with if you were in your right mind.

When you go shopping for homes, remember that you're vulnerable. Cupid may strike with his bow when you least expect it, causing you to fall in love - with the wrong house.

When you go shopping for homes, remember that you're vulnerable. Cupid may strike with his bow when you least expect it, causing you to fall in love - with the wrong house.

Oh, that won't happen to me, you say. But it can. You're a fool for love. If you want to keep your head and get the home that's really right for you and your household, follow these tips:

Shop Within Your Means

The wrong house will be too much trouble and money. Your lender will give you a price limit that you can comfortably afford based on your income and current debts. These are time-tested formulas that are designed to protect you from getting overextended and putting the bank's investment in jeopardy.

Work with a real estate professional

Look online and you'll fall in love with a home out of your league. You're welcome to look at homes online, but try to stay in your price range. If you look at homes that are more expensive than you can afford, you're bound to fall in love with more luxuries and space than you can comfortably afford. Share your wish list with a real estate professional, and let him or her preview homes for you.

Shop for the right-sized home, not the biggest

The wrong home is too big. While conventional wisdom says buy the most home that you can for the money, buying the biggest home you can isn't smart. Think about the operating costs of heating, cooling, cleaning and maintaining more square footage than you really need. Instead, think about how you actually use a home. Have a use for every space.

Shop For Your Lifestyle

The wrong home is perfect - for someone else. If you're single or travel a lot, you don't want to mow 10 acres. Consider a condominium or gated community. If you have kids, you may be more interested in neighborhoods with lots of options for kids to learn and do.

Consider the commute

The wrong home dazzles you with its elegance, but there's a price. Many of the newest homes offer the most amenities, but they're on cheaper land far from city centers. Ask yourself how long you'll spend commuting to your job every day to live in that particular community?

Don't Be Fooled By a Pretty Face

The wrong home isn't just pretty, it has to meet your needs. Where do the kids put their backpacks when they come home from school? Is it easy to let the dog outside and clean muddy paws when he comes back in? Do you have the space you need for your home office or art studio? Are there enough bathrooms for the morning rush?

Don't Overlook A Wallflower

Many homes are affordable because they're older and need work. Many times, cosmetic updates can turn a so-so home into a treasure. No home is perfect, so don't be side-tracked by ugly wallpaper.

Fall in love with the right house

The right house may not be the prettiest, biggest or the newest, but it will be the one that most suits the various needs of your household. When you're comparing homes think about your wish list and which home comes closest to meeting your price, number of bedrooms, condition, space, features and the amenities of the neighborhood.

Once you move in, you'll see that there's no falling in love that feels as good as knowing you made the right choice.

Have An Awesome Week!

THIS WEEK'S HOT HOME LISTING!

2670 Gay Street

2670 Gay Street

Price: $189,000 Beds: 3 Baths: 1 Half Baths: 1 Sq Ft: 1,924

In highly desirable North Gilham neighborhood! This home offers refinished hardwood floors, fresh interior paint, built-ins & lots of storage. Living rm w/ wood fireplace, family+dining rm w/ slider & propane stove opens to kitchen w/ pantry & eat-bar. Utility rm w/ half bath, additional rm could be office, plus storage/shop. RV parking ...

Why would sellers deliberately sabotage their chances of selling their homes? It doesn't make any sense, yet it happens all the time.

Why would sellers deliberately sabotage their chances of selling their homes? It doesn't make any sense, yet it happens all the time. Price: $529,000 Beds: 4 Baths: 4 Half Baths: 1 Sq Ft: 5,568

Price: $529,000 Beds: 4 Baths: 4 Half Baths: 1 Sq Ft: 5,568 With the housing marketing beginning to heat up again in the Eugene and Springfield market area, the climate for selling a home has never been better. If yoiu are considering putting your home on the market, there are a few things controlled by you that can make a huge difference on how long it takes your home to sell and at what price your home sells at. The following is an article from "Realty Times" that goes over some home selling dont's.

With the housing marketing beginning to heat up again in the Eugene and Springfield market area, the climate for selling a home has never been better. If yoiu are considering putting your home on the market, there are a few things controlled by you that can make a huge difference on how long it takes your home to sell and at what price your home sells at. The following is an article from "Realty Times" that goes over some home selling dont's. Price: $750,000 Beds: 4 Baths: 4 Half Baths: 1 Sq Ft: 4338

Price: $750,000 Beds: 4 Baths: 4 Half Baths: 1 Sq Ft: 4338

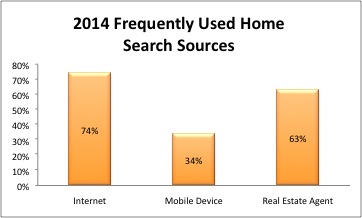

The most useful information for sellers and their agents is to be found in the section on the home search process. While the survey results are not significantly different from those of recent years, the trends continue. For example, this year 74 percent of buyers said that they used the internet frequently during the search process. In 2003 that number was only 42%. This past year 34% of buyers said that they frequently used a mobile or tablet application. That is a newer and growing phenomenon. 63% of buyers said that they frequently relied on a real estate agent for information.

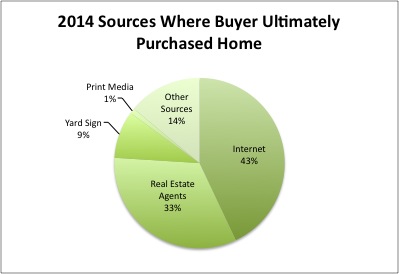

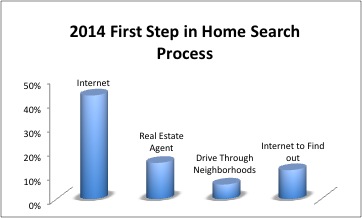

The most useful information for sellers and their agents is to be found in the section on the home search process. While the survey results are not significantly different from those of recent years, the trends continue. For example, this year 74 percent of buyers said that they used the internet frequently during the search process. In 2003 that number was only 42%. This past year 34% of buyers said that they frequently used a mobile or tablet application. That is a newer and growing phenomenon. 63% of buyers said that they frequently relied on a real estate agent for information. Forty-three percent of buyers went to the internet as the first step in the home search process. 15% contacted a real estate agent first, and 6% began by driving through neighborhoods looking for homes for sale. 12% first went online to find out about the process.

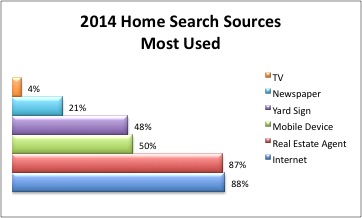

Forty-three percent of buyers went to the internet as the first step in the home search process. 15% contacted a real estate agent first, and 6% began by driving through neighborhoods looking for homes for sale. 12% first went online to find out about the process. Buyers use multiple sources of information in the process of looking for a home. Far and away the most used sources are on-line websites (88%) and real estate agents (87%). Mobile or tablet applications (50%) have replaced yard signs as the third most used source of information. Still though, 48% of buyers indicate that yard signs are one of their sources of information. Only 21% of buyers indicate that they used newspaper ads as an information source. A mere 4% garnered information from television.

Buyers use multiple sources of information in the process of looking for a home. Far and away the most used sources are on-line websites (88%) and real estate agents (87%). Mobile or tablet applications (50%) have replaced yard signs as the third most used source of information. Still though, 48% of buyers indicate that yard signs are one of their sources of information. Only 21% of buyers indicate that they used newspaper ads as an information source. A mere 4% garnered information from television.