Good Monday Morning!

In the Eugene and Springfield area, the housing market has become very tight for first-time home buyers. Lack of inventory, rising home prices, and now, increased mortgage interest rates have made the home search for first-time buyers even more difficult than it has over the past several years. This trend is not something that is just specific to Eugene and Springfield. The following article from "Realtor.com" addresses this national problem.

Soaring home prices and the shortage of properties on the market are taking a toll on buyers, particularly first-time buyers.

The share of first-time homeowners fell to just 29% of all existing home buyers in January, according to the most recent National Association of Realtors® report. That's down from 32% in December and 33% in January 2017.

The share of first-time homeowners fell to just 29% of all existing home buyers in January, according to the most recent National Association of Realtors® report. That's down from 32% in December and 33% in January 2017.

"First-time buyers are typically people with a tighter budget," says realtor.com® Senior Economist Joseph Kirchner, who worries this could further depress homeownership rates down the line. "They're looking for homes on the more affordable end of the market, but that is where the lack of homes is most severe."

Nationally, the dearth of inventory also drove down the number of existing homes sold, 5.38 million overall, in January. (Existing homes have previously been lived in.) Monthly sales dropped 3.2%, while annual sales decreased 4.8%.

(Realtor.com looked only at the seasonally adjusted numbers in the report. These have been smoothed out over 12 months to account for seasonal fluctuations.)

“There’s plenty of demand, but people just cannot find a home on the market that meets their needs and they can afford," Kirchner says. "It’s not a good start for the spring market. The shortage will continue.”

Across the country, there were 15.5% fewer existing homes in January selling for $250,000 or less compared with a year ago. Meanwhile, there were 25% more selling for $500,000 or more.

In January, sales of single-family homes, which are often the most sought-after properties, hit 4.76 million. That's a 3.8% fall from December and 4.8% from the same month a year earlier.

Condos and co-ops fared a bit better, as they're generally priced a little lower than single-family homes, with the number of monthly sales rising 1.6% in January to hit about 620,000. But that's down 4.6% from January 2017.

The median existing home price was $240,500 in January. That was a 2.4% drop from December but represented a 5.8% jump from January of the previous year. However, the cost was still substantially less than the median price of a newly constructed abode.

New homes cost a median $335,400 in December, according to the most recent joint report by the U.S. Census Bureau and U.S. Department of Housing and Urban Development. That's nearly 39.5% more than an existing home.

Around the country, higher prices and the lack of inventory took its toll. In January, the South had the most existing home sales, at about 2.26 million. However, that was still down 1.3% from December and was a 1.7% drop from January 2017.

The Midwest had the second most home sales, at 1.25 million, in January. That was down 6% from December and 3.8% lower than the same month last year.

There were 1.14 million existing homes sold in the West. That was a 5% drop from the previous month and a 9.5% fall from the previous year.

The Northeast had the fewest existing home sales, at just 730,000. That was also down, both by 1.4% month-over-month and 7.6% year-over-year.

Meanwhile, prices of existing homes were up in every region. They were the most expensive in the West, at a median $362,600 in January. That was a 8.8% jump over January 2017.

In the Northeast, median prices hit $269,100, up 6.8% annually. In the South, they were $208,200, up 4.3%, and in the Midwest, they were $188,000, up 8.7%.

In January, sales of single-family homes, which are often the most sought-after properties, hit 4.76 million. That's a 3.8% fall from December and 4.8% from the same month a year earlier.

Condos and co-ops fared a bit better, as they're generally priced a little lower than single-family homes, with the number of monthly sales rising 1.6% in January to hit about 620,000. But that's down 4.6% from January 2017.

The median existing home price was $240,500 in January. That was a 2.4% drop from December but represented a 5.8% jump from January of the previous year. However, the cost was still substantially less than the median price of a newly constructed abode.

New homes cost a median $335,400 in December, according to the most recent joint report by the U.S. Census Bureau and U.S. Department of Housing and Urban Development. That's nearly 39.5% more than an existing home.

"It’s very clear that too many markets right now are becoming less affordable and desperately need more new listings to calm the speedy price growth," NAR Chief Economist Lawrence Yun said in a statement.

Have an awesome week!

THIS WEEK'S HOT HOME LISTING!

Vineyard Hill Dr

Vineyard Hill Dr

Price: $230,000 Type: Bare Land Acres: 5

In The Vineyards! Gated entry, paved access, gorgeous views with meadow and trees. Great solar exposure potential for vineyard ground. Additional 6 acres to be deeded upon completion of approval for adjacent property.... View this property >>

AND HERE'S YOUR MONDAY MORNING COFFEE!!

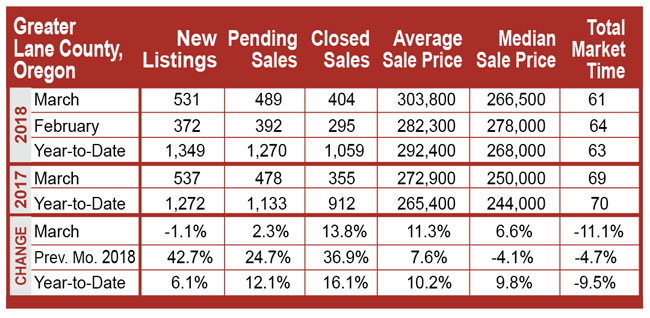

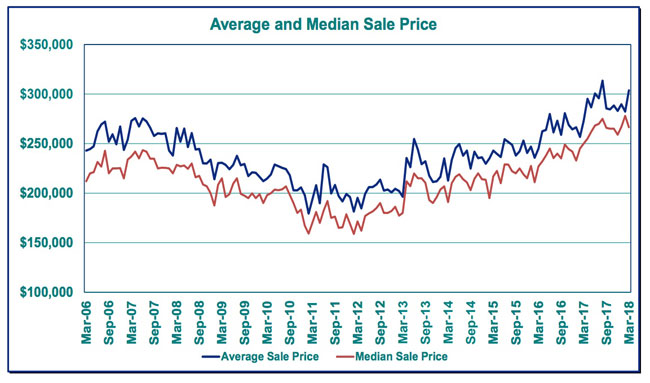

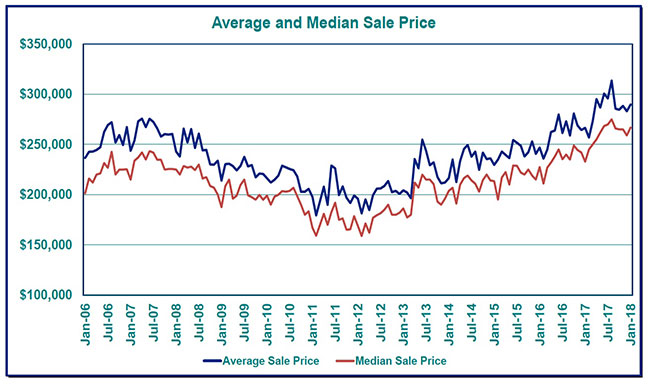

March home sale numbers are in for the Eugene and Springfield area and the sellers market trend continues. The inventory of homes for sale actually decreased from February, which is not normal and home prices continue to increase. This is not the best news for homebuyers, but continued good news for homesellers. My caution here is that with mortgage interest rates up and the continued increase in home prices, there will be a point where this market will shift and make a correction. That time could be sooner than later. Here is the March 2018 homes sales report.

March home sale numbers are in for the Eugene and Springfield area and the sellers market trend continues. The inventory of homes for sale actually decreased from February, which is not normal and home prices continue to increase. This is not the best news for homebuyers, but continued good news for homesellers. My caution here is that with mortgage interest rates up and the continued increase in home prices, there will be a point where this market will shift and make a correction. That time could be sooner than later. Here is the March 2018 homes sales report.

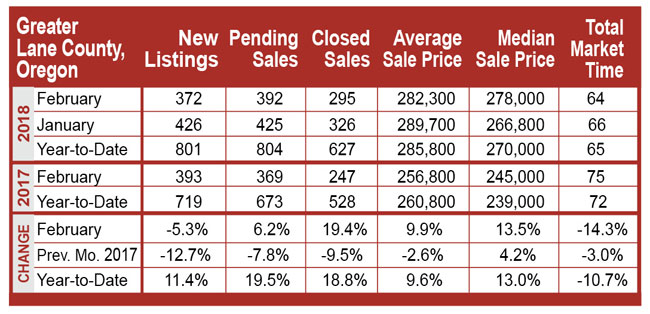

Lane County saw mixed activity this February, but most measures were ahead of February 2017. Closed sales (295) outpaced February 2017 (247) by 19.4% but fell 9.5% short of the 326 closings recorded last month in January 2018. It was the strongest February for closings in Lane County since 2007, when 305 were recorded.

Lane County saw mixed activity this February, but most measures were ahead of February 2017. Closed sales (295) outpaced February 2017 (247) by 19.4% but fell 9.5% short of the 326 closings recorded last month in January 2018. It was the strongest February for closings in Lane County since 2007, when 305 were recorded.

798 70th St

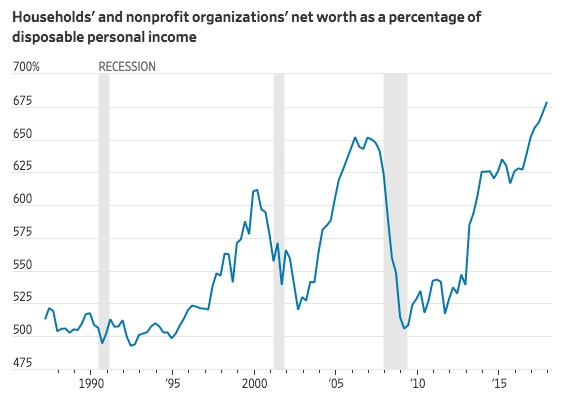

798 70th St  Yes, our national economy is taking off. Wages are up, employment is up and many economists say that this is just the beginning of a long improvement. The value of homes across the nation have steadily increased since the recession and have added to a large increase in national wealth.

Yes, our national economy is taking off. Wages are up, employment is up and many economists say that this is just the beginning of a long improvement. The value of homes across the nation have steadily increased since the recession and have added to a large increase in national wealth.

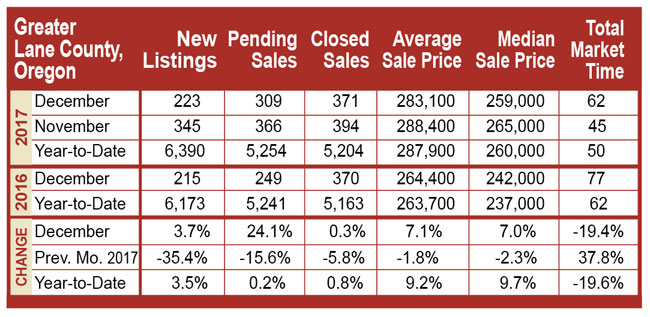

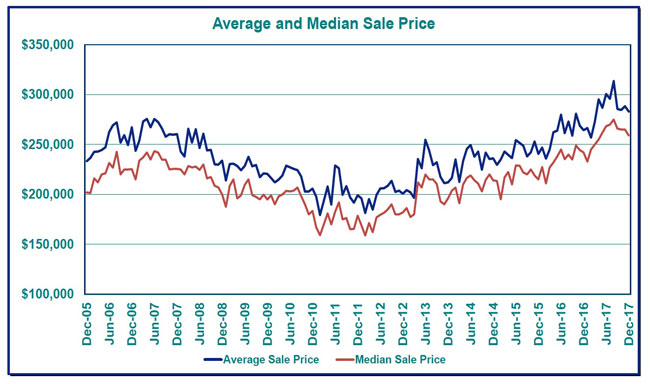

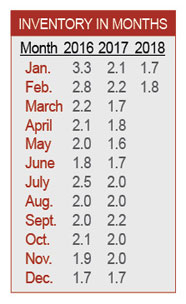

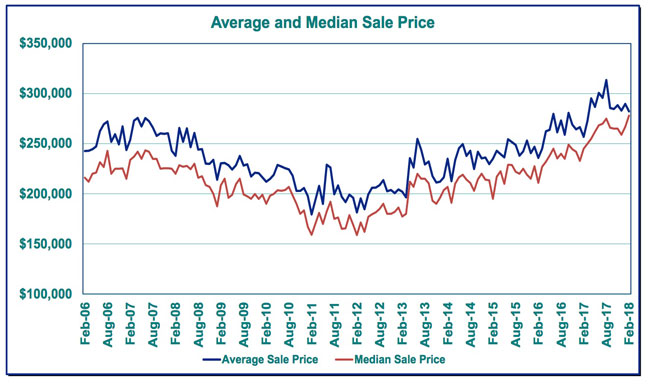

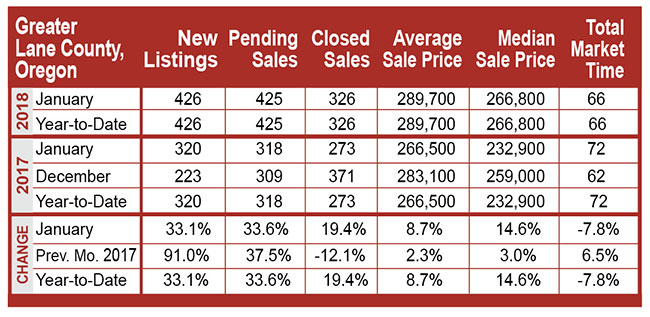

The Real Estate market in the Eugene and Springfield area was stronger in January of 2018 than in January of 2017. Both sales and new listings were up. The inventory of homes on the market remains low at 1.7 months and critically low in the first time buyer price ranges of $250,000 and below. Here are the home sale statistics for January 2018.

The Real Estate market in the Eugene and Springfield area was stronger in January of 2018 than in January of 2017. Both sales and new listings were up. The inventory of homes on the market remains low at 1.7 months and critically low in the first time buyer price ranges of $250,000 and below. Here are the home sale statistics for January 2018.

One of the largest problems that comes about during a home sale is the fact that there are typically seller paid repairs that need to be done. The majority of buyers are going to want both a pest and dry rot inspection and a whole home inspection completed as part of their purchase due diligence. From this inspection, there are typically some repair items that will come about and in most cases the buyer will want many of them taken care by the seller prior to the close of escrow. Negotiating these repairs during escrow can be nerve racking and can also sometimes create delays with closing. My suggestion to all of my sellers is to have their home inspected before we go on the market. This gives us a heads up for any potential issues and also allows the seller to repair major problems. Typically, this creates a much easier sale process. The followiong is and article from "US News" on why having a professional inspection prior to selling is a good thing to do.

One of the largest problems that comes about during a home sale is the fact that there are typically seller paid repairs that need to be done. The majority of buyers are going to want both a pest and dry rot inspection and a whole home inspection completed as part of their purchase due diligence. From this inspection, there are typically some repair items that will come about and in most cases the buyer will want many of them taken care by the seller prior to the close of escrow. Negotiating these repairs during escrow can be nerve racking and can also sometimes create delays with closing. My suggestion to all of my sellers is to have their home inspected before we go on the market. This gives us a heads up for any potential issues and also allows the seller to repair major problems. Typically, this creates a much easier sale process. The followiong is and article from "US News" on why having a professional inspection prior to selling is a good thing to do.

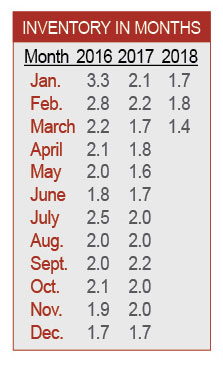

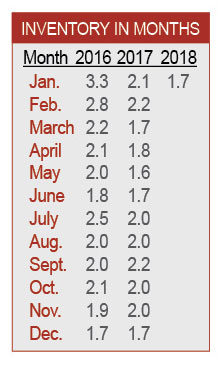

2018 has started out to be a challenging year for homebuyers in the Eugene and Springfield market area. The issue with the current market is certainly not demand. Our current home market problem stems from lack of inventory of homes for sale. This is especially true in the price ranges of below $300,000, where the high demand for housing exists. With a current inventory of less that 1.6 months, this shortage has left hundreds of would-be home buyers out in the dark. The lack of inventory and high demand has created such a shortage that when a home comes on the market that is priced well in the price range of high demand, there is typically a bidding war taking place. This of course is leading to the situation where many homes are now selling for above asking price. If this trend continues in 2018, it could be a challenging market for buyers.

2018 has started out to be a challenging year for homebuyers in the Eugene and Springfield market area. The issue with the current market is certainly not demand. Our current home market problem stems from lack of inventory of homes for sale. This is especially true in the price ranges of below $300,000, where the high demand for housing exists. With a current inventory of less that 1.6 months, this shortage has left hundreds of would-be home buyers out in the dark. The lack of inventory and high demand has created such a shortage that when a home comes on the market that is priced well in the price range of high demand, there is typically a bidding war taking place. This of course is leading to the situation where many homes are now selling for above asking price. If this trend continues in 2018, it could be a challenging market for buyers.